Nvidia has been one of the primary beneficiaries of the artificial intelligence (AI) megatrend. Its chips have been in high demand, which is powering tremendous revenue and earnings growth for the semiconductor company. It has made Nvidia one of the most highly valued companies in the world.

However, Nvidia isn’t the only company benefiting from the AI boom. The AI training models and applications that run on its chips reside in data centers. Those facilities are power-hungry buildings, especially when they support AI.

Because of that, power demand could surge in the coming years. That should benefit energy stocks, including the underappreciated natural gas sector. Here are a couple of ways to play the potential AI-fueled boom in natural gas demand.

Fueling the clean energy transition

Natural gas demand has grown steadily over the years. Several catalysts have fueled this growth, including replacing coal with the cleaner-burning fuel and rising LNG exports. Demand for gas could accelerate in the future, powered partly by AI data centers:

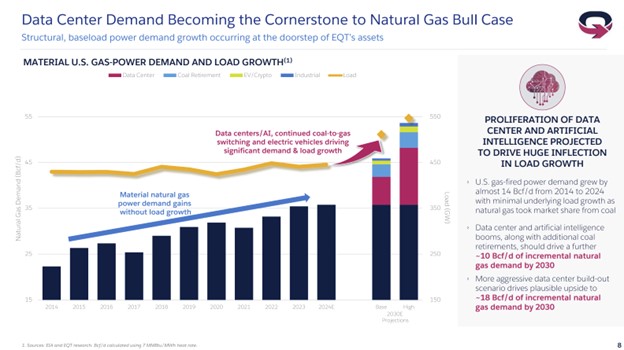

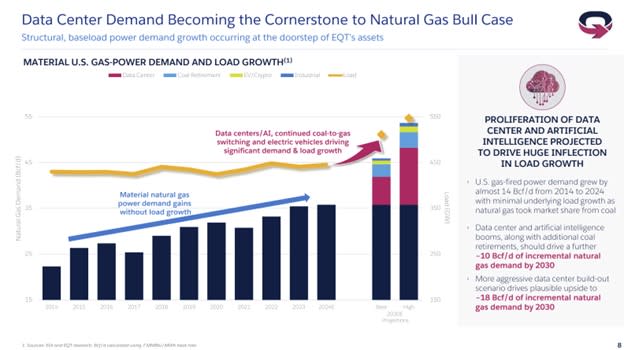

As that slide shows, data centers alone could drive an additional 10 billion to 18 billion cubic feet per day (bcf/d) of demand by 2030. That’s potentially more growth than the sector saw over the last decade.

Many companies in the natural gas industry should benefit from rising gas demand. One potential beneficiary is the country’s leading gas producer, EQT (NYSE: EQT). The company controls over 1.1 million net acres of land in the gas-rich Appalachian region (Pennsylvania, Ohio, and West Virginia). That large-scale position in one of the best gas-producing regions in the world enables it to produce gas at a very low cost ($1.36 per million cubic foot equivalent).

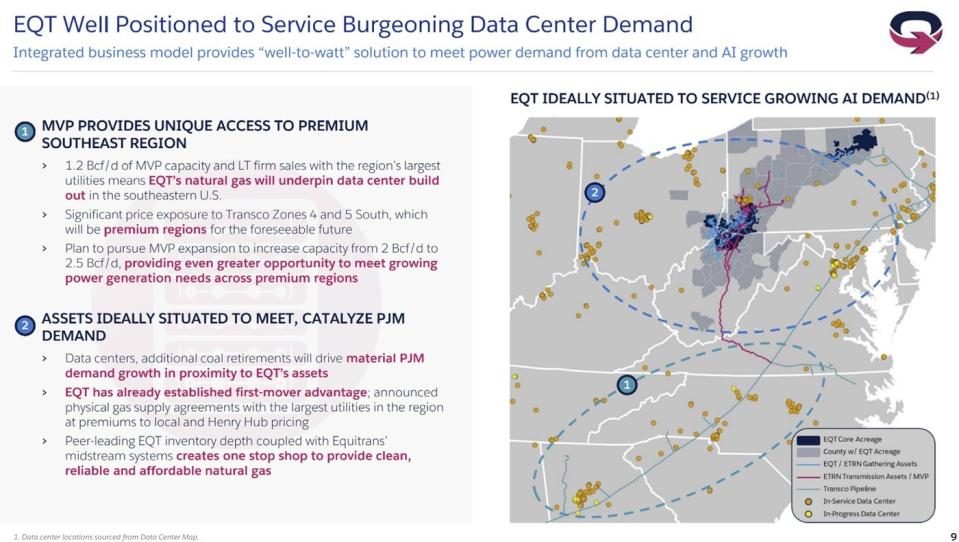

EQT is also ideally situated to supply gas to power data centers. The company has pipeline access (either those it will soon own via its Equitrans Midstream acquisition, or from contracts with third-party pipeline operators) to several data center clusters:

EQT should generate significant free cash flow in the coming years, fueled by growing gas demand and other catalysts like its pending Equitrans deal and contracts to supply new LNG export facilities. The company estimates that it could produce a cumulative $7.5 billion to more than $25 billion in free cash flow in the 2025 to 2029 period, assuming gas averages between $2.75 and $5 per MMBtu.

That high end is more likely if AI lives up to its potential. This robust cash flow will give it the funds to repay debt, pay dividends, and repurchase shares, which could fuel strong total returns for investors.

Transporting gas to demand centers

Natural gas pipeline companies are another potential big beneficiary of rising power demand fueled by AI data centers. That catalyst would increase transportation volumes on existing pipelines while providing them with new expansion opportunities.

One of the many potential beneficiaries is Williams (NYSE: WMB). The company operates the Transco pipeline, which runs along the East Coast, serving high-demand areas like Atlanta, Charlotte, North Carolina, and the capital region. Those areas are also hotbeds for data centers, which tend to be near major cities.

In particular, Transco could be a key to supplying gas to data centers in Virginia. Regional utility Dominion Energy expects power demand from facilities in its service area to grow by two and a half times over the next decade.

Williams currently has seven projects underway to expand Transco (and three more across its other major natural gas transmission pipelines). It has 30 more gas transmission pipeline projects in development. On top of that, the company has other gas infrastructure projects underway to grow its position in the Gulf of Mexico, Western U.S., and Northeast (where EQT operates).

These projects give Williams a lot of visibility. The pipeline giant expects to grow its earnings by 5% to 7% annually over the long term. That should give it the fuel to increase its high-yielding dividend (recently around 4.5%) by a similar rate. That combination of dividend income, earnings growth, and valuation upside potential could enable Williams to generate robust total returns in the coming years.

AI-fueled growth potential

Nvidia has been an early beneficiary of the AI boom. However, the technology will likely fuel growth for many other sectors, including natural gas. The market hasn’t yet fully appreciated the growth potential for the cleaner-burning fuel, which allows investors to get in early and potentially earn high-octane returns. EQT and Williams stand out as some of the biggest beneficiaries, given their proximity to where tech companies are building data centers.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,254!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,863!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $368,072!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of July 2, 2024

Matt DiLallo has positions in EQT. The Motley Fool has positions in and recommends EQT and Nvidia. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

Beyond Nvidia: AI Could Fuel High-Powered Growth for These Underappreciated Stocks. was originally published by The Motley Fool